{kind=link}

EVERY investor would like to find the perfect measurement tool to tell them when to get into, and out of, the stockmarket. The cyclically adjusted price-earnings ratio (CAPE), as calculated by Robert Shiller of Yale University, averages profits over ten years and is used by many as an important valuation indicator. Currently it shows that American shares have hitherto been more highly valued only in 1929 and the late 1990s, periods that were followed by big crashes.

That seems ominous. But as a paper by Dylan Grice and Gregor Obrecht of Calibrium, a Zurich-based private-investment office, makes clear, it is far from conclusive. The CAPE is not much use as a short-term indicator; it has been well above its long-term average for several years now, as it was in the late 1990s.

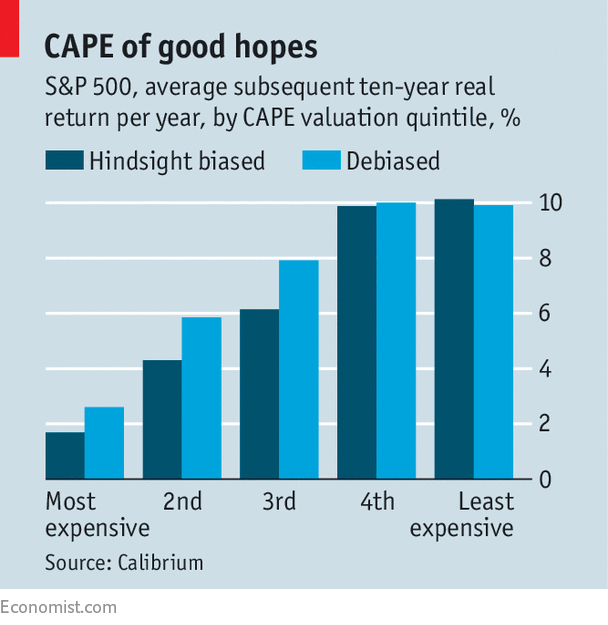

The main argument for the CAPE is a long-term one. If you divide all past CAPE values into quintiles, the annual returns earned over the subsequent decade by investing in equities when the CAPE was in its...Continue reading

from Business and finance http://www.economist.com/news/finance-and-economics/21731127-favoured-market-ratio-not-much-use-short-term-indicator-equity-valuations?fsrc=rss

No comments:

Post a Comment